Accrued expenses also may make it easier for companies to plan and strategize. Accrued expenses often yield more consistent financial results as companies can include recurring transactions in their financial reports that may not yet have been paid. In addition, accrued expenses may be a financial reporting requirement depending on the company and its Securities and Exchange Commission filing requirements. A utilities expense is defined as the cost a business incurs for the use of infrastructure provided by utility companies such as electricity, water supply, natural gas, sewage, and telephone services. The journal entry for utility expenses is straightforward.

The problem, therefore, is to separate cash items which should not be included in the working cash from those amounts which are necessary for the utility “to operate economically and efficiently”. The expense incurred on utilities by a company’s manufacturing operations falls under the category of its factory overhead. The expense is accumulated in a cost pool and then allotted to the units produced within a given period when the expense is incurred.

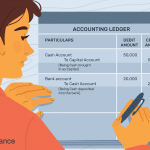

Journal Entries for recording an Accrued Expense.

Only noninterest-bearing customer deposits are to be considered. The public utility expense considers the provision of basic facilities necessary real estate bookkeeping for society. PwC refers to the US member firm or one of its subsidiaries or affiliates, and may sometimes refer to the PwC network.

In turn, the cost of rendering service is advanced to the utility by the utility’s suppliers and employees and by taxing agencies. As the average lag in payment of a utility’s expenses is generally longer than the lag in receiving revenues, the utility has funds which are not supplied by its investors available for its use. In determining the cash requirement, the only amounts which should be considered are the required minimum bank deposits that must be maintained and reasonable amounts of working funds. The determination of the amount of money required to pay expenses in advance of receipt of revenues is made by the lag study.

Then, supporting accounting staff analyze what transactions/invoices might not have been recorded by the AP team and book accrued expenses. In short, the accrual basis of accounting accelerates the recognition of utilities expenses in comparison to the cash basis of accounting. However, over the long term, the results under both methods will be approximately the same.

What is Utility Expense?

A/ Based upon an assumed 7.0% rate of return for the Electric department operation. Upgrading to a paid membership gives you access to our extensive collection of plug-and-play Templates designed to power your performance—as well as CFI’s full course catalog and accredited Certification Programs. Harold Averkamp (CPA, MBA) has worked as a university accounting instructor, accountant, and consultant for more than 25 years. He is the sole author of all the materials on AccountingCoach.com.

The fact that the amounts appear on the books of the utilities is not necessarily a satisfactory indication that the funds are used economically and efficiently to serve the customers. Therefore, analysis and evaluation of the reasonableness of these current asset accounts are required of the engineer to be able to develop the reasonable amounts to be included in the operational cash requirement. For telephone utilities, the requirement is equal to the average monthly operating expenses, exclusive of taxes and depreciation, multiplied by a certain number of months. Expenses should be allocated to toll service and local and miscellaneous service in proportion to total operating revenues received under each. Accrued expenses are prevalent during the end of an accounting period. A company often attempts to book as many actual invoices it can during an accounting period before closing its accounts payable ledger.

What is the journal entry for Utility Expense?

Therefore, the company is receiving the gas, electricity, etc. before it pays for them and has a liability until the bills are paid. Other cost varies for each business; a security guard’s salary is a utility expense in the case of banks and ATMs. All the maintenance expenses fall under utility expenses for all public utilities and services. Utility expense is the cost incurred in a reporting by using utilities like electricity, heat, sewage, waste disposable, and water. Sometimes, ongoing telephone and internet service expenditures also fall under the utility expense category.

- Accounting practices, tax laws, and regulations vary from jurisdiction to jurisdiction, so speak with a local accounting professional regarding your business.

- The state and federal corporation income taxes should be the estimated tax accruals that would result based upon the rate of return recommended by the staff’s rate or return expert.

- As indicated on the lower portion of Table 3-A, there is deducted from the amount of current assets accounts certain current liabilities which represent monies provided from sources other than the investors for the operation of the utility.

- To counter the argument that profit is advanced by the investor to the customer, it is proposed that it is the customer who actually pays the profit.

- Utility expense is the cost incurred in a reporting by using utilities like electricity, heat, sewage, waste disposable, and water.

A similar analysis of weighted average days is made of revenues by classes of customers to determine the average number of days that the utility has extended credit to its customers for the cost of service supplied by the utility. A company pays its employees’ salaries on the first day of the following month for services received in the prior month. So, employees that worked all of November will be paid in December. If on Dec. 31, the company’s income statement recognizes only the salary payments that have been made, the accrued expenses from the employees’ services for December will be omitted. Prepaid expenses are payments made in advance for goods and services that are expected to be provided or used in the future.

Examples of Accrued Expenses

It must be remembered that the cash requirement is not a measure of funds that the utility maintains for all purposes, such as for construction or for payment of dividends and interest. It is the amount that must be maintained for day-to-day operations. When the ratepayer pays his bill, he has compensated the investor for the interest on construction funds and a return on the investor’s capital; therefore construction cash, interest and dividends are not included in the cash requirement. In determining the deduction from the operational cash requirement, it is necessary to determine an approximate level of earnings on which the federal income tax accrual will be developed.

![]()

Government Accounting Standards Board (GASB) Statement No. 62 governs the recording of regulatory assets. According to the statement, regulatory assets are created when certain expenses are recognized as deferrals instead of period expenses. Accrual accounting measures a company’s performance and position by recognizing economic events regardless of when cash transactions occur, whereas cash accounting only records transactions when payment occurs. Accrual accounting presents a more accurate measure of a company’s transactions and events for each period. Cash basis accounting often results in the overstatement and understatement of income and account balances.

Debit and credit journal entries for the utilities expense paid

Since book depreciation expense is occurring uniformly day by day and accumulated depreciation is deducted from the rate base, the practice is to include depreciation provisions at zero lag days. Public utilities incur basic variable costs such as electricity, water, gas, internet, etc. Organizations using these utility records expenses based on their chosen accounting method, either accrual or cash basis. In the accrual system, the actual consumption of utilities is recorded, not just the received bills.

2023-08-01 NYSE:CEQP Press Release CRESTWOOD EQUITY … – Stockhouse Publishing

2023-08-01 NYSE:CEQP Press Release CRESTWOOD EQUITY ….

Posted: Tue, 01 Aug 2023 10:09:04 GMT [source]

Employee commissions, wages, and bonuses are accrued in the period they occur although the actual payment is made in the following period. As per the cash basis of accounting, the recorded amount relates to the cash paid for the given products or services within a mentioned period. Hence, the cash basis of accounting relies on the receipt of an invoice and only records the expense once the invoice has been paid. In the long term, the results under either of the two methods will be the same.

The following current liabilities accounts should be considered as deductions from the operational requirement. Except for cash, the amounts used in determining operational cash requirements for a given period are the average of month-end balances. Table 3-A, Sheet 1 of 5, illustrates the recommended format in the development of the operational cash requirement. Included therein are some of the selected balance sheet accounts which make up the operational cash requirement, as well as the deductions therefrom to obtain the working cash allowance.

![]()

It does not matter whether the utility supplier has sent an invoice to the company or not. If there is an amount that should be charged that is applicable to the previous month, it is charged to the current month. The utilities expense is on the basis of the amount used during an accounting period and can be included as part of the business’s operating expenses in the income statement. These expenses are relevant for running the business and are variable costs that change on the basis of consumption. Depending on the utility bill’s size, a business might maintain separate general ledger accounts for each utility, or combine them into a single utilities expense account. It is not out of place for a business to record these expenses when they are incurred.